Income statement explained is one of the most important topics every beginner should understand. If you want to learn stock market basics, business finance, or long-term investing, knowing how an income statement works is essential. In simple words, an income statement shows how much a company earns, how much it spends, and whether it makes profit or loss during a specific period. This beginner‑friendly guide explains the income statement in clear language with an easy example so that even non‑finance readers can understand it without confusion.

Meaning / Explanation of Income Statement

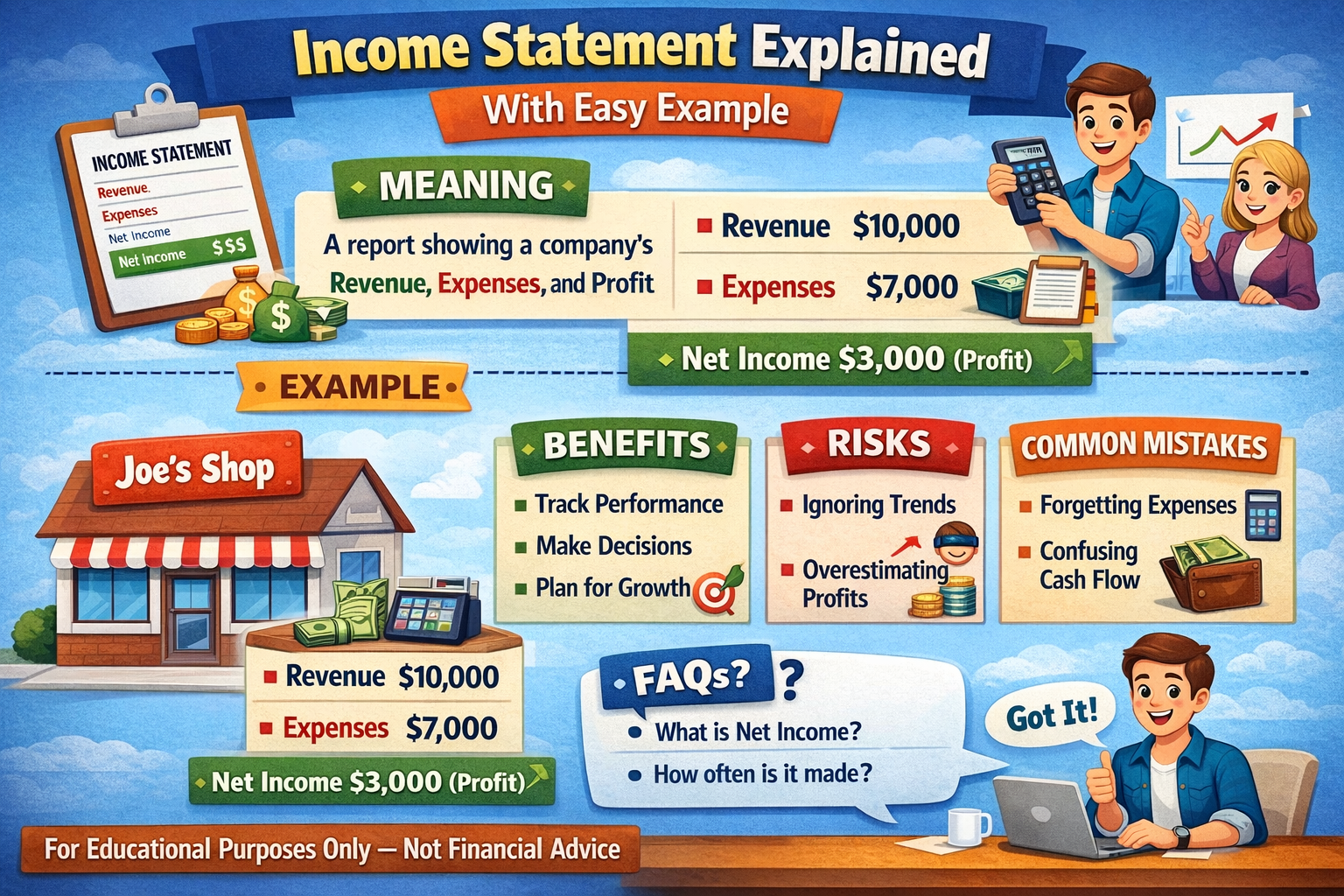

An income statement is a financial report that summarizes a company’s revenues, expenses, and profits or losses over a specific period, such as a month, quarter, or year. It is also called a Profit and Loss Statement (P&L) or Statement of Earnings. The main purpose of an income statement is to show whether a business is profitable and how efficiently it operates.

The structure of an income statement is simple. It starts with revenue (sales), subtracts different types of expenses, and ends with net profit or net loss. This flow helps investors, business owners, and analysts understand how money moves through a company. For beginners, the income statement answers three basic questions: How much did the company earn? How much did it spend? How much did it finally keep as profit?

Why Income Statement Matters

The income statement matters because it reveals the true financial performance of a business. Balance sheets show what a company owns and owes, but income statements show how well the company is actually performing over time.

Investors use income statements to decide whether a company is worth investing in. A consistently profitable company with growing revenue is often considered a strong investment, especially for long‑term investing. If you are new to investing, you may find these guides helpful:

Business owners use income statements to identify cost problems, improve profitability, and plan future strategies. Lenders and banks review income statements to assess whether a business can repay loans.

Key Parts of an Income Statement

Even though income statements can look complicated, most of them contain a few core sections that repeat across almost every business. Understanding these sections will help you read any company’s numbers with confidence.

- Revenue (Sales): The total money a company earns from selling goods or services before any expenses are deducted.

- Cost of Goods Sold (COGS): The direct costs related to producing goods or services, such as raw materials and direct labor.

- Gross Profit: Revenue minus COGS; it shows how much the company earns from its products after direct costs.

- Operating Expenses: Day‑to‑day running costs, such as rent, salaries, utilities, marketing, and admin expenses.

- Operating Profit (Operating Income or EBIT): Gross profit minus operating expenses; it shows profit from core operations before interest and tax.

- Other Income / Other Expenses: Non‑operating items like interest income, interest expense, or one‑time gains and losses.

- Taxes: Income tax paid to the government based on taxable profit.

- Net Profit (Net Income): The final profit after all expenses, interest, and taxes are deducted; this is often called the bottom line.

How Income Statement Works (With Easy Example)

Let us understand how the income statement works using a simple example of a small business called ABC Traders. This example will make the income statement explained in a step‑by‑step way.

Step 1: Revenue (Sales)

ABC Traders sells electronic accessories. In one year, the company earns ₹10,00,000 from sales. This amount is called Revenue or Top Line.

Step 2: Cost of Goods Sold (COGS)

To sell these products, ABC Traders spends ₹6,00,000 on raw materials, manufacturing, and packaging. This is called Cost of Goods Sold.

Gross Profit = Revenue – COGS

₹10,00,000 – ₹6,00,000 = ₹4,00,000

Step 3: Operating Expenses

Operating expenses include rent, salaries, electricity, marketing, and administrative costs. ABC Traders spends ₹2,00,000 on these expenses.

Operating Profit = Gross Profit – Operating Expenses

₹4,00,000 – ₹2,00,000 = ₹2,00,000

Step 4: Other Expenses and Taxes

The company pays ₹50,000 as interest and ₹30,000 as taxes.

Net Profit = Operating Profit – Other Expenses – Taxes

₹2,00,000 – ₹80,000 = ₹1,20,000

This ₹1,20,000 is the Net Profit of ABC Traders and is what ultimately belongs to the owners after covering all costs.

Mini Income Statement of ABC Traders

Here is how the same information looks in a simplified income statement format.

ABC Traders - Income Statement for the Year Revenue (Sales) ₹10,00,000 Less: Cost of Goods Sold (COGS) ₹ 6,00,000 -------------------------------------------- Gross Profit ₹ 4,00,000 Less: Operating Expenses ₹ 2,00,000 -------------------------------------------- Operating Profit (EBIT) ₹ 2,00,000 Less: Interest Expense ₹ 50,000 Less: Taxes ₹ 30,000 -------------------------------------------- Net Profit ₹ 1,20,000

Important Profit Margins (Simple Ratios)

Numbers become even more powerful when you convert them into simple percentages called margins. These profit margins help you compare companies of different sizes very easily.

- Gross Profit Margin = (Gross Profit ÷ Revenue) × 100

- Operating Profit Margin = (Operating Profit ÷ Revenue) × 100

- Net Profit Margin = (Net Profit ÷ Revenue) × 100

For ABC Traders:

- Gross Profit Margin = ₹4,00,000 ÷ ₹10,00,000 = 40%

- Operating Profit Margin = ₹2,00,000 ÷ ₹10,00,000 = 20%

- Net Profit Margin = ₹1,20,000 ÷ ₹10,00,000 = 12%

Even if two companies have the same revenue, the one with higher margins usually runs the business more efficiently and keeps more profit from its sales.

Single-Step vs Multi-Step Income Statement

In practice, companies can present their income statement in slightly different layouts, but two common styles are single‑step and multi‑step. Both formats follow the same idea of showing revenue, expenses, and profit.

- Single‑Step Income Statement: All revenues are added together and all expenses are added together. The company then subtracts total expenses from total revenues to get net income. This style is simple but less detailed.

- Multi‑Step Income Statement: Revenues and expenses are grouped into sections like gross profit, operating income, and non‑operating items. This format clearly shows core business performance and is more useful for analysis.

For serious investing and business analysis, the multi‑step format is more helpful because it highlights operating profit separately from financing and tax effects.

Benefits of Income Statement

- Helps evaluate company profitability.

- Easy to understand and compare.

- Useful for investment decisions.

- Supports long‑term financial planning.

- Shows trends in revenue and expenses.

Understanding income statements also helps investors appreciate concepts like the power of compounding when profits grow year after year:

Power of Compounding Explained

Risks / Limitations of Income Statement

While the income statement is powerful, it also has some limitations that every beginner should know.

- Does not show cash flow.

- Can be manipulated using accounting methods.

- One‑time gains may mislead investors.

- Does not reflect future performance.

For example, a company might show a high profit because it sold some old assets, but that does not mean its regular core business is strong. Similarly, profit can look healthy even when the business is struggling with cash because revenue is recorded on an accrual basis, not when money actually comes into the bank.

How Investors Use Income Statements

Investors and analysts use income statements along with other financial statements to judge whether a company is fundamentally strong. They do not look at just one year but study several years to see consistent performance.

- Trend Analysis: Checking whether revenue and net profit are growing steadily over 3–5 years.

- Margin Analysis: Studying gross, operating, and net profit margins to see if the company is maintaining or improving efficiency.

- Quality of Earnings: Understanding whether profits come mainly from core operations or from one‑time items like asset sales or accounting adjustments.

- Comparison with Peers: Comparing margins and growth with other companies in the same industry instead of random companies in different sectors.

By combining this analysis with the balance sheet and cash flow statement, investors can form a more complete picture of the business. For more detailed theory, readers can also check educational resources such as the income statement overview on Investopedia.

Difference Between Income Statement and Other Statements

The income statement is only one part of the full financial picture. To avoid confusion, it helps to know how it differs from the other two key financial statements.

| Aspect | Income Statement | Balance Sheet | Cash Flow Statement |

|---|---|---|---|

| What it shows | Revenues, expenses, and profit or loss for a period. | Assets, liabilities, and equity at a specific date. | Actual cash inflows and outflows during a period. |

| Main question answered | “Was the business profitable?” | “What does the business own and owe right now?” | “How much cash came in and went out?” |

| Time focus | Covers a period (month, quarter, year). | Snapshot on a particular date. | Covers a period, similar to income statement. |

| Accounting vs cash | Prepared on accrual basis, may not match cash movement. | Shows balances after accounting adjustments. | Shows actual cash movement only. |

Common Mistakes / Myths

- Assuming profit means cash in hand: A company can report profit but still face cash shortages due to delayed customer payments or heavy investments.

- Ignoring operating margins: Focusing only on net profit without checking operating profit can hide weak core operations.

- Comparing different industries blindly: Profit margins in software, retail, banking, and manufacturing can be very different, so comparisons should be within the same industry.

- Focusing only on revenue growth: High sales growth without matching profit growth may indicate poor cost control or aggressive discounting.

Simple Tips to Read an Income Statement

Beginners often feel overwhelmed by all the line items, but a few simple steps can make analysis much easier.

- Start with revenue and see whether it is growing compared to previous periods.

- Look at COGS and calculate gross profit and gross margin to understand product‑level profitability.

- Check operating expenses and operating profit to judge how efficient the core business is.

- Review interest expense and taxes to see how much profit is eaten away by loans and government dues.

- Finally, look at net profit, net margin, and any notes about one‑time items or adjustments.

With practice, this process becomes quick and helps you avoid emotional decisions in the stock market. The more often you apply it, the more natural the income statement explained here will feel.

FAQ Section

1. What is an income statement?

An income statement shows a company’s revenues, expenses, and profits over a period. It is also known as a profit and loss statement or statement of earnings.

2. Is income statement important for beginners?

Yes, it is one of the easiest financial statements to understand and is a great starting point for learning business and investing. Once you master the income statement explained in this article, other statements become easier.

3. How often is an income statement prepared?

Usually quarterly and annually for listed companies, though some businesses also prepare monthly internal income statements for monitoring performance.

4. What is net profit?

Net profit is the final profit after all expenses, interest, and taxes are deducted from total revenue. It is often called the bottom line of the income statement.

5. Can income statements be trusted?

They are generally reliable for most companies but should always be analyzed along with the balance sheet, cash flow statement, and management quality.

6. What is EPS on the income statement?

EPS (Earnings Per Share) tells how much profit is available for each share of stock, calculated as net income divided by the number of outstanding shares.

7. Do all businesses use the same income statement format?

The basic structure is similar, but service companies, manufacturers, and banks may present some line items differently based on their business model.

8. What is the difference between operating profit and net profit?

Operating profit shows profit from core business activities, while net profit is after including interest, taxes, and other non‑operating items.

Conclusion

The income statement is a powerful tool for understanding a company’s financial performance. For beginners, learning how to read and analyze an income statement builds a strong foundation for investing and business decisions.

When combined with long‑term investing principles, income statements can help identify financially strong companies that create sustainable wealth over time. Always analyze income statements carefully and use them as part of a broader financial strategy that also includes other financial statements and qualitative factors.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Always consult a qualified financial advisor before investing.